Two Roads to the Same Destination

Real estate has built more generational wealth than almost any other asset class in history. The question in today’s market isn’t whether real estate deserves a place in your investment portfolio — it almost certainly does. The real question is how you get there. Do you buy a physical property and manage it the traditional way? — Real Estate Investment Trusts — to access the same market without owning a single square foot of actual space?

Both routes have passionate advocates. Both have produced real returns for real investors. And both carry risks that brochures and sales pitches conveniently understate. This article gives you the honest, unfiltered comparison — what REIT investing actually looks like in practice, what direct property ownership truly costs, and which option makes more sense depending on your goals, budget, and appetite for involvement.

To be clear from the start: this isn’t a question with one universal right answer. It’s a question with a right answer for you — and finding that answer requires understanding the mechanics, trade-offs, and real-world numbers on both sides of the equation.

What Exactly Is a Real Estate Investment Trust?

Before comparing the two, it helps to understand what a real estate investment trust actually is—not the textbook definition, but what it means practically for someone putting money in.

A real estate investment trust is a company or trust that owns, operates, or finances income-generating real estate assets. Think large-scale commercial properties—office parks, shopping malls, logistics warehouses, hospitals, data centers, and hotel portfolios. Instead of one investor owning one building, thousands of investors collectively own a share of dozens or hundreds of properties spread across multiple cities, managed by a professional team.

The structure is straightforward: you buy units of a listed REIT on a stock exchange—in India, the NSE or BSE—and you receive regular dividend distributions, typically quarterly, from the rental income those properties generate. By regulation, a REIT in India must distribute at least 90% of its net distributable cash flow to unitholders. That’s not optional—it’s a legal requirement, which is part of what makes REIT investing an inherently income-oriented strategy.

In India, the market currently has three listed: Embassy Office Parks REIT (the country’s first), Mindspace Business Parks REIT, and Brookfield India Real Estate Investment Trust. A fourth option—Nexus Select Trust—focuses on retail assets. The Nifty REITs & InvITs Index, which tracks their collective performance, has delivered a 1-year return of 16.41% and a CAGR of 11.42% since its inception in July 2019. These are not insignificant numbers.

Think of it as operating somewhat like real estate mutual funds — they pool investor capital, deploy it across a diversified portfolio of properties, and return income to participants. Unlike traditional mutual funds, however, REITs own actual physical real estate assets rather than stocks or bonds, and their returns are directly tied to rental income and property valuations rather than equity market performance. While some real estate mutual funds invest in REIT stocks and real estate sector equities, a listed REIT gives you direct exposure to the underlying property cash flows — a meaningful distinction.

The Case for REIT Investing

1. Accessibility: Real Estate for Practically Anyone

The most immediate advantage of REIT investing is the dramatic reduction in the barrier to entry. Buying a 2BHK apartment in Hyderabad, Bangalore, or Mumbai requires anywhere from ₹40 lakh to several crores — plus stamp duty, registration fees, interiors, and maintenance reserves. By contrast, you can begin REIT investing with as little as ₹10,000–₹15,000 in the secondary market. You participate in income from Grade-A commercial real estate that a retail investor could never otherwise afford to own, at a fraction of the capital commitment.

2. Liquidity: When Life Doesn't Wait for a Property Sale

Physical property is famously illiquid. Selling an apartment — even in a hot market — can take weeks to months, involves brokers, stamp duty negotiations, and a buyer chain that can collapse at any point. Selling REIT units is as simple as placing a trade through any SEBI-registered broker. SEBI Regulations. In most market conditions, your position is liquidated within a trading session. For investors who might need access to funds on shorter timelines, this difference is not trivial — it’s fundamental.

3. Passive Income Without Passive Headaches

One of the most underappreciated aspects of reit investing is what it removes from your life, not just what it adds. There are no tenant calls at 11 PM about a leaking pipe. No hunting for maintenance contractors. No dealing with rent disputes or navigating the legal process of eviction. No vacancy months where your asset sits idle and still costs you money. The Real Estate Investment Trust structure puts professional asset managers in charge of every operational decision while you collect distributions and monitor your portfolio from a dashboard.

4. Diversification Built Into the Structure

REITs own dozens or hundreds of properties across multiple geographies and tenant types. A single REIT might have offices leased to Microsoft, Amazon, and HDFC across Hyderabad, Pune, and Mumbai simultaneously. If one tenant vacates or one city’s commercial market softens, the impact is cushioned by the rest of the portfolio. A direct property investor with one apartment in one city has exactly zero of this diversification — their entire position lives or dies with a single asset in a single market.

5. Regulatory Transparency

In India, REITs are regulated by SEBI under the Real Estate Investment Trusts Regulations, 2014. This means mandatory quarterly disclosures, audited financials, independent valuations of the underlying assets, and defined governance structures. For investors who want regulatory oversight and transparency built into their investment vehicle, listed Real Estate Investment Trusts offer a level of institutional accountability that most direct property transactions — especially in secondary markets — simply cannot match.

The Nifty REITs & InvITs Index has delivered a CAGR of 11.42% since inception in July 2019, combining price return with dividend distributions. That’s a meaningful long-term data point for REIT investing in the Indian context.

The Case for Buying Physical Property

1. Leverage: The Multiplier That Changes the Math

The single biggest financial advantage that direct property ownership has over REIT investing is leverage. When you buy a ₹60 lakh apartment with a 20% down payment (₹12 lakh) and an 80% home loan, you control a ₹60 lakh asset with ₹12 lakh of your own capital. If that property appreciates by 15% to ₹69 lakh, your actual return on capital deployed is 75% — not 15%. REITs offer no equivalent leverage mechanism. You own exactly as many rupees of real estate as you put in.

This leverage effect is why many of India’s largest personal wealth stories have been built on direct property — not through superior selection, but through the compounding power of borrowed capital amplifying moderate appreciation into exceptional absolute returns.

2. Tangibility and Emotional Anchoring

There is something psychologically powerful about owning a physical asset. You can see it, visit it, renovate it, and use it personally if circumstances change. A property in Gachibowli or Banjara Hills is not just an investment — it’s a home for your family, a legacy for your children, a stable address in a city you know. This emotional dimension of direct real estate ownership is genuinely real and shouldn’t be dismissed as irrational. Many investors sleep more soundly owning a physical flat than a collection of REIT units on a brokerage platform.

3. Capital Appreciation Potential

In cities like Hyderabad, where the right micro-markets have delivered 70%+ appreciation over five years, direct property has periodically outpaced what listed REITs have returned in terms of pure capital gains. While REIT unit prices do appreciate with underlying property values and market sentiment, the appreciation trajectory of a well-chosen residential asset in an IT corridor — bought ahead of infrastructure development — can be exceptional in a way that a diversified REIT portfolio rarely is.

4. Control and Customization

When you own property directly, you make every significant decision: which tenant, at what rent, when to sell, whether to renovate, how to structure the lease. For investors who want hands-on involvement in their wealth-building process, this control is a genuine advantage. REIT investing is inherently passive — management decisions are made entirely by the trust’s professional team, for better or worse.

5. Personal Use Optionality

A direct property investment can double as your primary residence, a family member’s home, or a holiday property. This optionality — the ability to use the asset yourself if investment conditions change — has tangible value that a portfolio of REIT units cannot replicate.

The Risks: What Nobody Puts in the Brochure

Risks of REIT Investing

Despite the structural advantages, REIT investing carries real risks that demand clear-eyed acknowledgment. REIT unit prices are listed on exchanges and therefore subject to market sentiment — during broad equity sell-offs, REIT units can fall in price even when the underlying properties are performing well and distributions remain stable. This market volatility is the price of liquidity.

Distribution income is not guaranteed. If occupancy rates fall — due to economic slowdowns, corporate downsizing, or shifts in how companies use office space (as demonstrated during the COVID-19 period) — distributions can be reduced. Additionally, Real Estate Investment Trusts are typically leveraged at the fund level, meaning the trust itself borrows to acquire properties. If interest rates rise sharply, financing costs increase and distributions can be pressured.

In India specifically, the REIT market remains relatively young and thin, with limited options and lower secondary market depth compared to equity markets. The tax treatment of REIT distributions — which are taxable at the investor’s applicable income tax slab rate — can also make net returns less attractive for higher-income investors.

Risks of Direct Property Investment

Direct property carries its own set of well-documented hazards. Concentration risk is perhaps the most significant — most retail investors own one or two properties at most, meaning their entire real estate position is exposed to a single location’s demand-supply dynamics, local governance decisions, and infrastructure trajectory.

Hidden costs erode returns in ways that paper calculations rarely capture. Maintenance and upkeep, property tax, society charges, brokerage, registration, stamp duty, interior costs, and vacancy periods between tenants can collectively reduce actual net yield from the headline 3–5% toward 1.5–2.5% in real terms. Legal and title risks — particularly in under-construction or semi-urban properties — can in extreme cases result in partial or total capital loss.

Illiquidity is also a genuine constraint. Unlike REITs vs physical real estate where the comparison favors REITs on exit flexibility, a physical property in a soft market can take months to sell and may require price concessions that significantly impact realized returns.

When evaluating REITs vs. real estate on a like-for-like basis, always model the net yield after costs — not the gross yield. For direct property, deduct management fees, maintenance, vacancy, and taxes. For REITs, consider the tax treatment of distributions at your applicable slab rate.

Head-to-Head: The Full Comparison

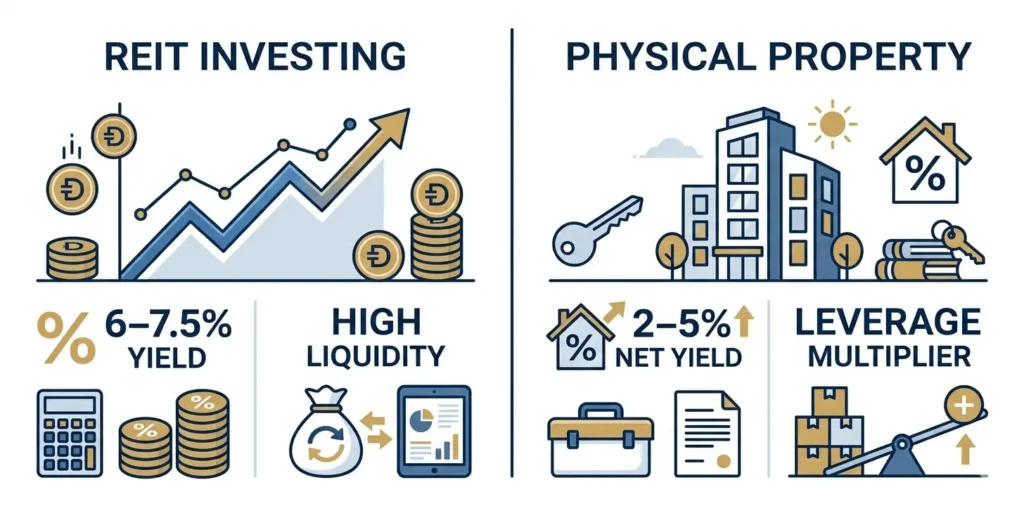

Here’s how REITs vs. physical real estate stack up across the parameters that matter most to serious investors:

|

Parameter |

REITs |

Physical Property |

|

Minimum Entry |

₹10,000 (REIT units) |

₹35 lakh+ (apartment) |

|

Liquidity |

High—sell like shares |

Low—months to sell |

|

Rental Yield |

6–7.5% (distributions) |

2–5% net |

|

Capital Appreciation |

Moderate (unit price) |

High (direct property) |

|

Leverage (Home Loan) |

Not available |

Up to 80% LTV |

|

Management |

Fully professional |

Self or hired manager |

|

Diversification |

Across sectors & cities |

Single asset, location |

|

Regulation |

SEBI-regulated |

RERA (varies by state) |

|

Tax on Income |

As per investor slab |

30% TDS above ₹2.4L rent |

|

Effort Required |

Passive—near zero |

Active management needed |

How to Invest: Getting Started With Each Option

How to Invest in REITs

Getting started with REIT investing in India is straightforward. You need a Demat account with any SEBI-registered broker — Zerodha, Upstox, HDFC Securities, ICICI Direct, or any equivalent platform. Search for listed REITs by name (Embassy Office Parks REIT, Mindspace Business Parks REIT, Brookfield India Real Estate Investment Trust, or Nexus Select Trust) on the exchange. Buy units at market price, just like you would purchase equity shares. Distributions are credited directly to your linked bank account on a quarterly basis.

For investors who prefer indirect exposure through real estate mutual funds — funds that invest primarily in REIT stocks and real estate sector equities rather than the underlying properties directly — several AMCs in India offer this option. However, note that real estate mutual funds carry equity market correlation that differs from direct unit ownership, and their expense ratios add a layer of cost. Pure investing through exchange-listed units is generally the cleaner, more direct route for property-specific exposure.

The emerging Small and Medium REIT (SM REIT) framework from SEBI is also expanding the landscape, enabling fractional ownership of smaller assets through regulated structures with minimum investments starting around ₹10 lakh. Platforms like PropShare and hBits are building products on this framework, offering a middle ground between full units and direct property ownership.

How to Invest in Physical Property

Direct property investment begins with defining your target zone, budget, and purpose — rental income, capital appreciation, or both. Verify the project’s RERA registration in your state before committing to anything. In Telangana, this means checking the TGRERA portal. Secure pre-approval on your home loan to understand your real purchasing power. Engage a registered property lawyer for title verification on any transaction above ₹25–30 lakh.

Factor in the full cost of ownership before calculating projected returns: stamp duty (4–6% of transaction value in most states), registration fees, brokerage (1–2%), interiors, maintenance deposits, and the first few months of potential vacancy. Build a realistic return model that accounts for net yield — not gross rental income — against your total capital deployed including all acquisition costs.

Which Is Safer?

Safety in investing is context-dependent, but some principles apply broadly. On a regulatory and structural basis, listed REITs operating under SEBI oversight offer a level of investor protection — mandatory disclosures, independent valuations, distribution requirements — that direct property transactions in India’s fragmented market often cannot match. Legal title risk, fraudulent developers, and documentation irregularities are real hazards in direct property that simply don’t exist in the listed REIT universe.

On a capital preservation basis, however, physical property has historically shown lower short-term volatility than listed REIT unit prices, which move with market sentiment. A property’s “price” only becomes apparent when you try to sell it — the absence of daily mark-to-market can feel safer even when the underlying value is fluctuating just as much.

The honest answer: They are structurally safer due to regulatory oversight, diversification, and the elimination of concentration risk. Direct property is operationally simpler for investors who want a tangible asset they can touch and understand. Neither is risk-free, and the notion of “safe” real estate investment — whether through a Real Estate Investment Trust or a flat purchase — has always been a simplification that deserves scrutiny.

Which Is More Profitable?

This is the question everyone actually wants answered, and the data-honest response is: it depends on your time horizon, your use of leverage, and the specific assets involved.

On a pure yield basis, listed Indian REITs have delivered total returns (price appreciation + distributions) in the 11–16% range annually since inception, with distributions averaging 6–7.5%. Direct residential property in India’s best-performing micro-markets has delivered capital appreciation of 7–15% annually in peak periods, with net rental yields of 2–4% after costs, for total returns in the 10–18% range in the top quartile of locations.

Where direct property outperforms significantly is when leverage is applied effectively. A 20% down payment on a well-chosen property in a high-growth corridor — financed by a home loan at 8.5–9% — can generate returns on equity deployed that dramatically exceed anything available through reit investing. The reverse is also true: a poorly chosen property in a weak location, burdened by vacancy and hidden costs, will underperform a simple REIT investment almost every time.

The most defensible answer is this: for most investors without the capital, time, or expertise to identify and manage direct property effectively, a lower-effort path to real estate returns. For investors who can identify great locations, manage tenants competently, and use leverage responsibly, direct property — particularly in India’s best-performing cities — offers greater total return potential over a long enough horizon.

A data point worth remembering: ₹1 lakh invested in Indian real estate 20 years ago would have grown to approximately ₹4.4 lakh (CAGR ~7.7%). The Nifty 50 over the same period delivered a CAGR of approximately 14–16%. while newer in India, have outperformed both residential property yield and inflation in their first five years of listing.

The Verdict: Who Should Choose What

Choose REIT Investing If You:

Have limited capital (under ₹5 lakh) and want real estate market exposure. Value liquidity and the ability to exit quickly. Want passive income without property management responsibilities. Are an NRI or remote investor who can’t physically oversee a property. Want to diversify a portfolio that already includes direct property. Are new to real estate investing and want a regulated, lower-complexity starting point.

Choose Direct Property If You:

Have the capital for a down payment and qualify for a competitive home loan. Are investing in a specific high-growth corridor where you have genuine local knowledge. Can manage or supervise property management over a 5–10 year horizon. Want the optionality of personal use or intergenerational wealth transfer. Are comfortable with illiquidity in exchange for leverage-amplified returns.

Or: Do Both

The most sophisticated approach — and the one increasingly favored by serious real estate investors — is to use REIT investing for diversified, liquid, income-generating exposure while holding one or two direct properties for leverage-amplified appreciation and personal use optionality. These two strategies are not mutually exclusive, and their risk profiles are complementary enough that combining them makes genuine portfolio sense

FAQs

Q1. What is a Real Estate Investment Trust (REIT) in simple terms?

A Real Estate Investment Trust is a company that owns and manages income-generating properties — offices, malls, warehouses — and distributes at least 90% of its earnings to investors as dividends. You buy units on a stock exchange, just like shares, and earn proportional rental income without owning any physical property.

Q2. Is REIT investing safe?

REIT investing in India is regulated by SEBI, which mandates mandatory disclosures, independent valuations, and governance standards. It eliminates legal title risk and concentration risk associated with direct property. However, listed REIT unit prices are subject to stock market volatility, and distributions can be impacted by occupancy rates or rising interest rates. Structurally safer than most direct property transactions — but not risk-free.

Q3. How do REITs compare to real estate mutual funds?

Real estate mutual funds typically invest in stocks of real estate companies and REIT units through a fund structure, adding a management expense layer. Listed REITs give you direct exposure to underlying property cash flows with lower costs and more transparency. For pure real estate income exposure, listed REIT units are generally preferred over real estate mutual funds by informed investors.

Q4. What is the minimum investment for REIT investing in India?

You can start reit investing from approximately ₹10,000–₹15,000 in the secondary market for listed REITs on NSE/BSE. The SM REIT framework enables fractional commercial property ownership from ₹10 lakh. Both are dramatically lower entry points than direct residential property, which typically starts at ₹35–40 lakh in most major Indian cities.

Q5. What returns can I expect from REIT investing vs buying property?

REIT investing in India has delivered total returns (price + distributions) of approximately 11–16% annually since listing, with yields of 6–7.5%. Direct residential property in top-tier Indian cities has delivered capital appreciation of 7–15% annually in high-growth corridors, with 2–5% net rental yield. Direct property with leverage can outperform significantly — but also amplifies losses if the asset underperforms.

Q6. Which Indian REITs are available to invest in right now?

Currently listed REITs in India include: Embassy Office Parks REIT, Mindspace Business Parks REIT, Brookfield India Real Estate Investment Trust, and Nexus Select Trust (retail assets). All are listed on NSE and BSE and accessible through any standard Demat account.

Q7. Can I use a home loan to invest in REITs the way I can for property?

No. Home loans are not available for REIT unit purchases. This is the most significant structural disadvantage of reit investing versus direct property — you cannot use leverage to amplify your returns. Every rupee of REIT exposure requires a full rupee of your own capital, while direct property allows up to 80% bank financing.

Q8. What are the tax implications of REIT investing in India?

REIT distributions are generally taxable at the investor’s applicable income tax slab rate. STCG (holding ≤ 1 year) on unit sales is taxed at 15%; LTCG (holding > 1 year, gains above ₹1 lakh) is taxed at 10% without indexation — similar to equity taxation. For direct property, rental income is taxed at slab rates and capital gains at 20% with indexation for LTCG (holding > 2 years).

Q9. Is it possible to invest in real estate online through REITs?

Yes — REIT investing is entirely digital. Open a Demat account with any SEBI-registered online broker, search for listed REIT units by name, buy at market price, and receive distributions to your bank account. No site visits, no agents, no paperwork beyond your standard KYC. It is one of the most accessible and transparent ways to invest in real estate online available in India today.

Q10. Should I invest in a REIT or buy property in Hyderabad specifically?

If your budget is under ₹15 lakh and you want real estate exposure now: REIT investing is the clear practical choice. If you have ₹40 lakh+, a clear location strategy (Gachibowli, Kondapur, Tellapur), and a 5–7 year horizon: direct property in Hyderabad’s IT corridors has delivered compelling returns and still offers meaningful upside in emerging zones. The optimal answer for many investors is both — REITs for diversified yield, direct property for leveraged appreciation in a city with strong structural fundamentals.

The best investment isn’t the one that sounds most impressive at a dinner party. It’s the one that fits your capital, your timeline, and your honest tolerance for complexity. REITs and physical property are both legitimate, powerful wealth-building tools — understand both, and use each where it earns its place in your portfolio.