Rules Written in Brick and Mortar

Real estate has minted more millionaires than perhaps any other asset class in history. But walk into any property market without a framework, and you will discover something uncomfortable: good intentions are not a strategy. The difference between a smart investor who builds lasting wealth and one who circles endlessly from bad deal to bad deal often comes down to whether they understand—and actually live by—the golden rules of property investment.

These are not the kind of rules that get outdated with the next interest rate cycle. They predate the internet, the smartphone, and the concept of fractional investing. The golden rules of property investment are structural principles, carved from the collective experience of every investor who has ever bought a building, watched a neighborhood transform, suffered a vacancy, or woken up one morning to discover their asset is worth three times what they paid for it. They are the constant in a market that changes constantly.

Whether you are just starting your journey in property investing or you are an experienced player looking to pressure-test your approach, these five rules are the litmus test for every major decision you will make. Apply them consistently, and you build a portfolio. Ignore them, and you build regrets. Check out the documents you’d require to invest in real estate in Hyderabad.

Rule 1: Location Is Not Just Important — It Is Everything

Every experienced player in property investment will tell you that the most dangerous three words in real estate are not ‘prices might fall’ — they are ‘location can improve.’ It might. But a smart investor never builds a strategy around possibility when they can build it around probability. And the probability of a prime location retaining demand is about as close to a certainty as real estate offers.

Location governs everything downstream: the quality of tenants your property for investment will attract, the rental income it can command, the speed at which it appreciates, and, crucially, the speed at which you can sell it when you want to exit. A well-located property in a market with poor timing will still find buyers. A poorly located property in a strong market will still struggle. That asymmetry is the entire argument for location as the first of the golden rules of property investment.

What Makes a Location Prime?

The most useful framework is to evaluate location on four dimensions simultaneously:

Employment anchors:

Proximity to large, stable employers—IT parks, hospitals, universities, financial districts—creates a self-renewing pool of quality tenants. These clusters generate demand regardless of broader economic weather.

Infrastructure trajectory:

Look at where roads, metro lines, ring roads, and expressways are being built — not where they already exist. Smart investors in property investing buy ahead of the infrastructure curve, not after.

Social infrastructure quality:

Good schools, hospitals, retail, and recreational spaces within accessible distance are what tenants and buyers actually search for. These amenities also protect value during market downturns.

Supply constraints:

The best locations are ones where supply is structurally limited — either by geography, regulation, or established density. Scarcity of supply is what turns moderate demand into meaningful price appreciation over time.

— Barbara Corcoran, one of America’s most celebrated real estate investors, built her entire empire on one principle: buy in the right place, let the tenant cover your costs, and let time do the work. The location does not just determine rental income — it determines how much of your risk the market eliminates for you over a long hold.

Rule 2: Positive Cash Flow Is Not Optional — It Is Oxygen

There is a tempting narrative in property investment that goes like this: buy a great property in a great location, accept slightly negative monthly cash flow, and wait for appreciation to compensate over time. This narrative has destroyed more investment portfolios than poor market timing ever has.

Cash flow — the money left over after every expense is paid — is the oxygen of property investing. Without it, even a fundamentally excellent asset becomes unsustainable. Mortgages do not pause during vacancy. Insurance premiums do not negotiate around your cash shortage. Maintenance requirements do not wait for convenient timing. A smart investor understands that positive cash flow is not a bonus outcome — it is the baseline requirement that makes long-term property for investment viable at all.

Understanding Your Numbers

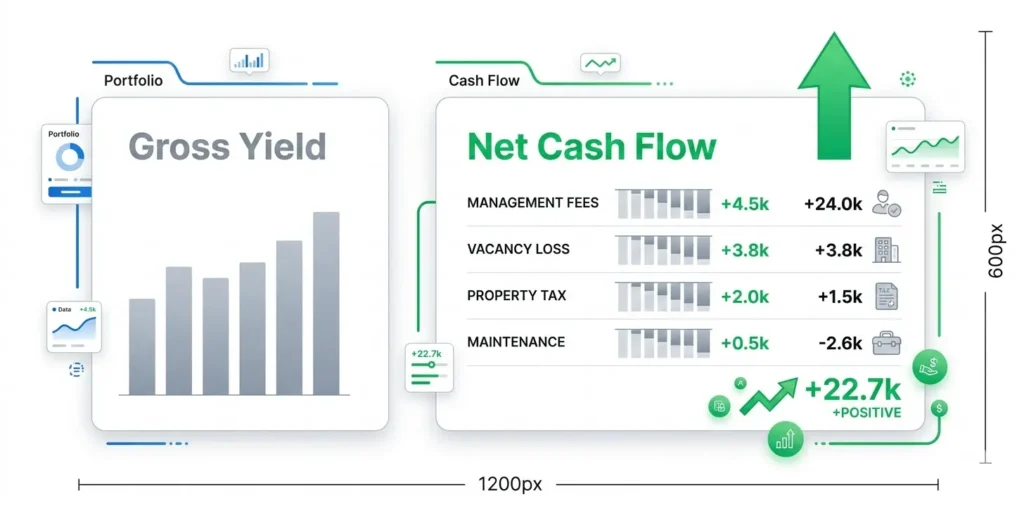

The benchmark most professional investors in property investing use is a target Return on Investment (ROI) of between 8% and 12% annually. This accounts for rental income after expenses, with a net operating income that comfortably covers mortgage payments, property tax, insurance, maintenance reserves, and vacancy provisions. Industry data suggests that budgeting for at least a 5–7% vacancy rate annually is prudent—in a national average context, properties can sit untenanted for one to three months between good tenants.

Two useful quick-screening tools: the 1% Rule suggests that monthly rent should equal at least 1% of the property’s purchase price to ensure positive cash flow. The 5% Rule suggests that the total acquisition cost, including renovations, should not exceed five times the property’s annual rental income. Neither replaces detailed financial modelling, but both allow a smart investor to filter opportunities rapidly and focus analysis on genuinely viable assets. Rental property cash flow and ROI benchmarks for 2025.

Target Annual ROI

8%–12% (professional benchmark, 2025)

National Vacancy Rate

7.0% (Q2 2025) — budget conservatively

1% Quick Screen

Monthly rent = at least 1% of purchase price

Net yield after property management fees, maintenance, vacancy, and taxes is typically 1–1.5% below the headline gross yield figure. Always model net returns — never gross. A property showing 5% gross yield may deliver only 3.2% net, which changes the investment case entirely.

Rule 3: Never Skip Due Diligence — Not Even Once

Every investor who has ever suffered a serious loss in property investment has a version of the same story. It starts with excitement—a property that checks most of the boxes, a price that feels right, and a vendor who seems credible. And it ends with a discovery: a legal encumbrance that was never disclosed, a structural defect the inspection did not catch, a zoning restriction that eliminates the planned use, or a title issue that surfaces three years after purchase. The golden rules of property investment exist precisely because human nature—optimism bias, deal excitement, and fear of missing out—reliably causes people to skip the one step that would have revealed the problem.

Due diligence in property for investment is not a bureaucratic hurdle. It is the systematic process of converting excitement into information—replacing what you hope is true about a property with what you know is true. And the cost of doing it properly (legal fees, professional inspection, independent valuation) is always—without a single exception—lower than the cost of skipping it. Real estate investment strategies and due diligence frameworks.

The Non-Negotiable Checklist for Every Acquisition

✓ Title verification through a registered property lawyer to confirm clean ownership with no encumbrances, disputes, or pending litigation.

✓ Regulatory approval check — confirm the property or project has all required statutory approvals from the relevant planning authorities. Never purchase an unapproved layout or an under-construction project without verified regulatory clearances.

✓ Physical and structural inspection by an independent professional, not a vendor-recommended inspector.

✓ Independent rental market analysis to verify the rental income projections provided by the seller or broker are realistic and achievable in the current market.

✓ RERA or equivalent registration check for under-construction projects, confirming the developer’s legal standing and compliance with real estate regulations.

he five minutes it takes to verify a property’s legal status online — whether through RERA portals, planning authority records, or municipal approval databases — have saved investors from losses running into crores. Make it the first thing you do after expressing interest, not the last.

Rule 4: Use Leverage Wisely and Think in Decades, Not Years

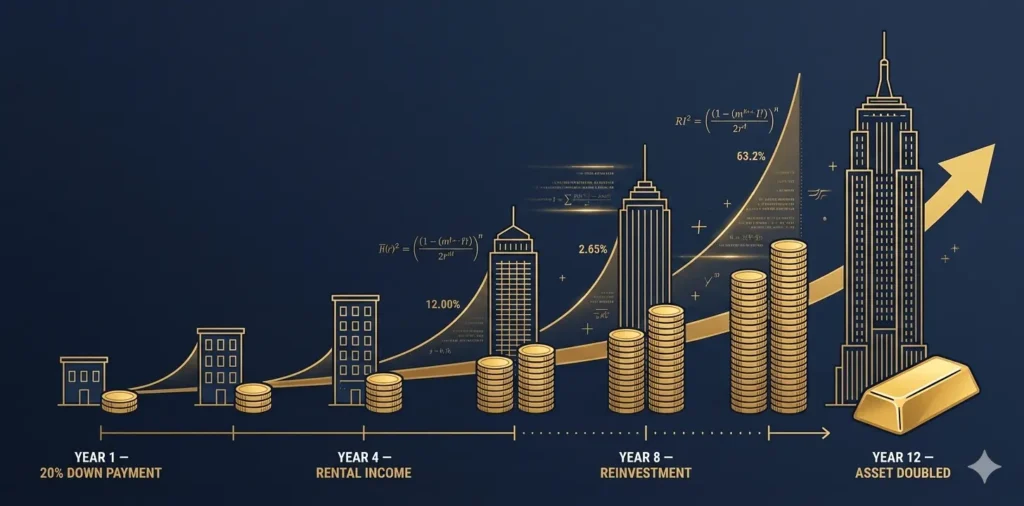

One of the most powerful advantages that property investment holds over almost every other asset class is the ability to use leverage—borrowed capital—to control a much larger asset with a relatively small equity position. A smart investor who buys a property with a 20% down payment and 80% bank financing controls 100% of an asset while deploying only 20% of their own capital. If that property appreciates by 10%, their return on capital deployed is 50%. That amplification is the engine of real estate wealth creation that no other mainstream investment vehicle replicates as accessibly.

But leverage is only a golden rule of property investment when it is applied responsibly. Borrowing against property at rates higher than the income it generates, or stretching into too many simultaneous acquisitions without adequate cash reserves, transforms leverage from a wealth accelerator into a financial liability. The smart investor structures their leverage so that rental income comfortably services the debt—and still provides a cash reserve buffer for the unexpected. Comfortable does not mean barely adequate. It means genuinely comfortable, accounting for a meaningful vacancy period or maintenance event.

The Long Game Is Not Optional

Warren Buffett’s observation that the best holding period for an investment is forever was not an abstract philosophical position. It was a direct observation about how compounding works in assets that generate income and appreciate over time. In property investing, the two most common regrets are “Why did I not buy sooner?” and “Why did I sell too early?” Both reflect the same underlying reality: real estate rewards patience in a way that very few other investments do.

Capital growth at a modest 6–8% per year doubles an asset’s value in 9–12 years. Rental income compounds alongside it, gradually shifting from covering costs to generating meaningful surplus cash flow. A property for investment purchased today in a fundamentally sound location may feel ordinary for the first few years — and extraordinary by year twelve. This is not luck. It is the mechanical outcome of applying the golden rules of property investment with patience and discipline. The five golden rules of property investing and compound growth.

Leverage Example

20% down on a 10% appreciating property = 50% return on capital deployed

Compounding at 6% annual growth

Asset value doubles in approximately 12 years

Compounding at 8% annual growth

Asset value doubles in approximately 9 years

The opencorp.au study on property investment fundamentals found that capital growth builds empires — owning a portfolio that increases in value by even 6% annually means you are on track for financial freedom, particularly as compound growth comes into play. But cash flow must also be factored in, or you risk losing grip of your assets entirely.

Rule 5: Professional Property Management Protects Every Gain

There is a version of property investment that looks excellent on a spreadsheet and feels exhausting in practice. Self-managing multiple properties — handling tenant calls, chasing late payments, coordinating repairs, staying compliant with evolving landlord regulations, managing vacancy periods, and conducting periodic inspections — is a full-time job that most investors neither planned for nor want. And when it is done poorly, it directly erodes the returns that made the investment attractive in the first place.

Professional property management is not an optional luxury for large portfolios. It is the infrastructure that allows a smart investor to scale beyond a single property without scaling their personal workload proportionally. A good property management partner handles tenant sourcing and screening, rent collection, maintenance coordination, financial reporting, regulatory compliance, and vacancy minimization—all of which directly impact the ROI of your property for investment. Their fee (typically 8–10% of rental income) is one of the most efficient investments in your portfolio’s performance.

What Good Property Management Delivers

The financial impact of professional property management is measurable. Rigorous tenant screening reduces late payments and property damage. Systematic lease management reduces vacancy periods between tenants. Proactive maintenance prevents small issues from becoming expensive capital problems. Regular market rent reviews ensure the property is not underpriced relative to what comparable units are achieving. Each of these disciplines—applied consistently—compounds into meaningfully higher net returns over a five-to-ten-year holding period. maximizing ROI on rental properties in 2025.

The most resilient portfolios in property investing are built not just on good acquisition decisions but on excellent operational discipline after acquisition. This is why the final of the golden rules of property investment is not about buying—it is about what you do after you buy. The asset is the vehicle. Property management is the engine. Both need to work for the journey to reach its destination.

According to Buildium’s 2025 property management research, the property management practices that most directly improve ROI are online rent collection (reduces AR days), systematic tenant screening (reduces delinquency), and proactive vacancy marketing (reduces time between tenants). Together, these practices can add 1–2% to the net annual yield on a well-run portfolio.

Bonus: Choosing Your Property Investment Strategy

The five golden rules of property investment apply regardless of which strategy you pursue — but the strategy itself determines your timeline, your capital requirements, and your day-to-day involvement. The four primary approaches to property for investment are:

Buy and Hold:

The cornerstone of long-term wealth building. Buy a well-located, cash-flow-positive property and hold it for 7–15 years, letting appreciation and compounding rental income do their work. The lowest-friction, most reliable path for investors who want to build wealth steadily without active involvement.

Fix and Flip:

Buy undervalued properties, renovate them to a higher standard, and sell at a profit. Requires strong market knowledge, accurate cost estimation, and active project management. Profitable in rising markets — risky in flat or declining ones.

Buy, Renovate, Rent, Refinance, Repeat (BRRRR):

A capital-recycling strategy that allows a smart investor to deploy the same equity across multiple acquisitions by pulling it back out via refinancing after renovation. Powerful if executed correctly; demanding in terms of time and expertise.

REIT or Fractional Investing:

For investors who want real estate exposure without property management responsibility. REITs deliver diversified income from large-scale commercial property, while fractional platforms enable smaller-ticket participation in specific assets. Lower return ceiling than direct ownership, but dramatically lower effort and entry capital. Top Real Estate Investment Strategies for 2025

Conclusion: Five Rules, One Outcome

The golden rules of property investment are not complicated. They are not the exclusive knowledge of industry insiders or billionaire developers. They are available to every investor willing to apply them with consistency and patience. Buy the right location. Ensure positive cash flow from the start. Never skip due diligence. Use leverage wisely and hold for the long term. Invest in professional property management as the operational backbone of your portfolio.

What makes property investing genuinely powerful — and genuinely unforgiving — is that the rules are simple, but discipline is not. The deals that violate these principles always seem compelling in the moment. The pressure to act quickly, the fear of missing out, the easy narrative about why this particular exception is justified — these are the forces that the golden rules of property investment are specifically designed to protect you from.

Apply them once and you make a good investment. Apply them consistently across every acquisition and you build a portfolio. Apply them for long enough and you build the kind of financial position that does not require you to make another decision if you choose not to. That is the real outcome of property investment done properly — not a quick win, but the compound effect of disciplined decisions, made correctly, repeated over time.

The rules have not changed. The market has. The rules win, every time.

Frequently Asked Questions (FAQs)

Q1. What are the golden rules of property investment in simple terms?

The golden rules of property investment are five core principles every serious investor follows: (1) Prioritise location above all else. (2) Ensure positive cash flow before acquiring any asset. (3) Never skip due diligence — legal, structural, and financial. (4) Use leverage responsibly and hold assets for the long term. (5) Invest in professional property management to protect and maximise returns after acquisition. Together, they form the operational framework that separates successful property investing from expensive guesswork.

Q2. How important is cash flow vs capital growth in property investment?

Both matter—and they work together. Capital growth builds long-term wealth and portfolio equity. Positive cash flow keeps you solvent while you wait for that growth to materialize. A smart investor never sacrifices one entirely for the other. The ideal property for investment delivers sufficient rental income to cover all costs and provide a monthly surplus while being located in an area with a credible appreciation trajectory. Chasing pure capital growth at the cost of negative cash flow is one of the most common and costly mistakes in property investing.

Q3. What does property management actually include and why does it matter?

Property management covers tenant sourcing and screening, rent collection, maintenance coordination, lease management, financial reporting, regulatory compliance, and vacancy minimisation. It matters because each of these functions directly impacts the net yield and long-term condition of your asset. Weak property management leads to higher vacancy, more frequent bad debt, deferred maintenance that compounds into capital costs, and below-market rents that are never reviewed. Professional property management at 8–10% of rental income is consistently one of the highest-ROI expenditures in a property investment portfolio.

Q4. How much money do I need to start property investing?

The entry point for direct property investing depends on your target market. In most Indian tier-1 cities, a residential apartment in a growth corridor requires a minimum down payment of approximately 20% of the purchase price — which on a ₹50 lakh property means ₹10 lakh of your own capital. Beyond the down payment, budget for stamp duty, registration, legal fees, and initial maintenance reserves. For those with less capital, fractional property for investment platforms and listed REITs offer real estate exposure from as little as ₹10,000–₹10 lakh depending on the instrument. The golden rules of property investment apply equally regardless of entry capital.

Q5. Is leveraging with a home loan always a good idea in property investment?

Leverage is powerful when rental income comfortably covers the debt service with margin to spare. It becomes dangerous when the property runs cash-flow negative — meaning you are paying out of pocket every month in the hope of future appreciation. The test for healthy leverage: your net rental income (after all expenses including property management fees) should cover your EMI and leave a buffer. If it does not, you are speculating on appreciation rather than investing based on fundamentals — a meaningful risk distinction that every smart investor takes seriously.

Q6. How do I know if a location is a good one for property investment?

Evaluate four factors: (1) Employment anchors — large, stable employers within commutable distance. (2) Infrastructure development — metro lines, expressways, and road projects planned or under construction nearby. (3) Social infrastructure quality — schools, hospitals, and retail within accessible range. (4) Supply constraints — limited new land or planning restrictions that cap future supply. A location that scores well across all four is the foundation for reliable property investment returns. The single biggest mistake in property investing is paying a premium for a location based on what it is today, rather than what the fundamentals suggest it will become.

Q7. What is the 1% rule in property investing?

The 1% rule is a quick screening tool used in property investing to assess whether a rental property is likely to be cash-flow positive. It states that a property for investment should generate monthly rental income equal to at least 1% of its total purchase price. A property purchased for ₹60 lakh should therefore bring in at least ₹60,000 per month in rent to pass the test. The rule is a filter, not a final decision tool — properties that fail it rarely make good property investment candidates, while those that pass still require full financial modelling before commitment.

Q8. Why should I hire a property manager instead of managing my investment myself?

Self-management of a single rental property is feasible for some investors. Beyond that, the time, expertise, and regulatory knowledge required make professional property management the more economically rational choice for most. Consider: a good property management firm reduces vacancy through faster tenant placement, reduces bad debt through rigorous screening, prevents maintenance cost escalation through proactive upkeep, and ensures rent is reviewed to market rates regularly. The aggregate value of these services — typically delivered for 8–10% of rental income — almost always exceeds their cost in measurable ROI improvement over a 3–5 year period.